In March 2026, the government of the Democratic Republic of the Congo (DRC) approved the sale of Congolese mining company Chemaf to US company Virtus Minerals, in a transaction commonly reported at over USD 700 million. This approval, just a year after a competing USD 1.4 billion offer by Chinese company Norin Mining was rejected, was widely described as a landmark victory for the United States in its pushback against China for the global control of critical minerals.

While China remains Kinshasa’s dominant mining partner by a large margin, the deal signals a shift in the DRC’s economic and geopolitical alliances, with direct consequences for the legal and political framework governing mining investments.

This Lex Africana Deep Dive examines that shift, focusing on the DRC’s role in global supply chains, its “minerals for infrastructure” partnership with China, the evolution of its legal regime toward greater resource sovereignty, the recent “minerals for security” agreement with the United States, and what this all means for the overall framework and legal protection of mining investments in the DRC.

THE DRC’S POSITION IN GLOBAL MINERAL SUPPLY: REASSERTING BARGAINING POWER

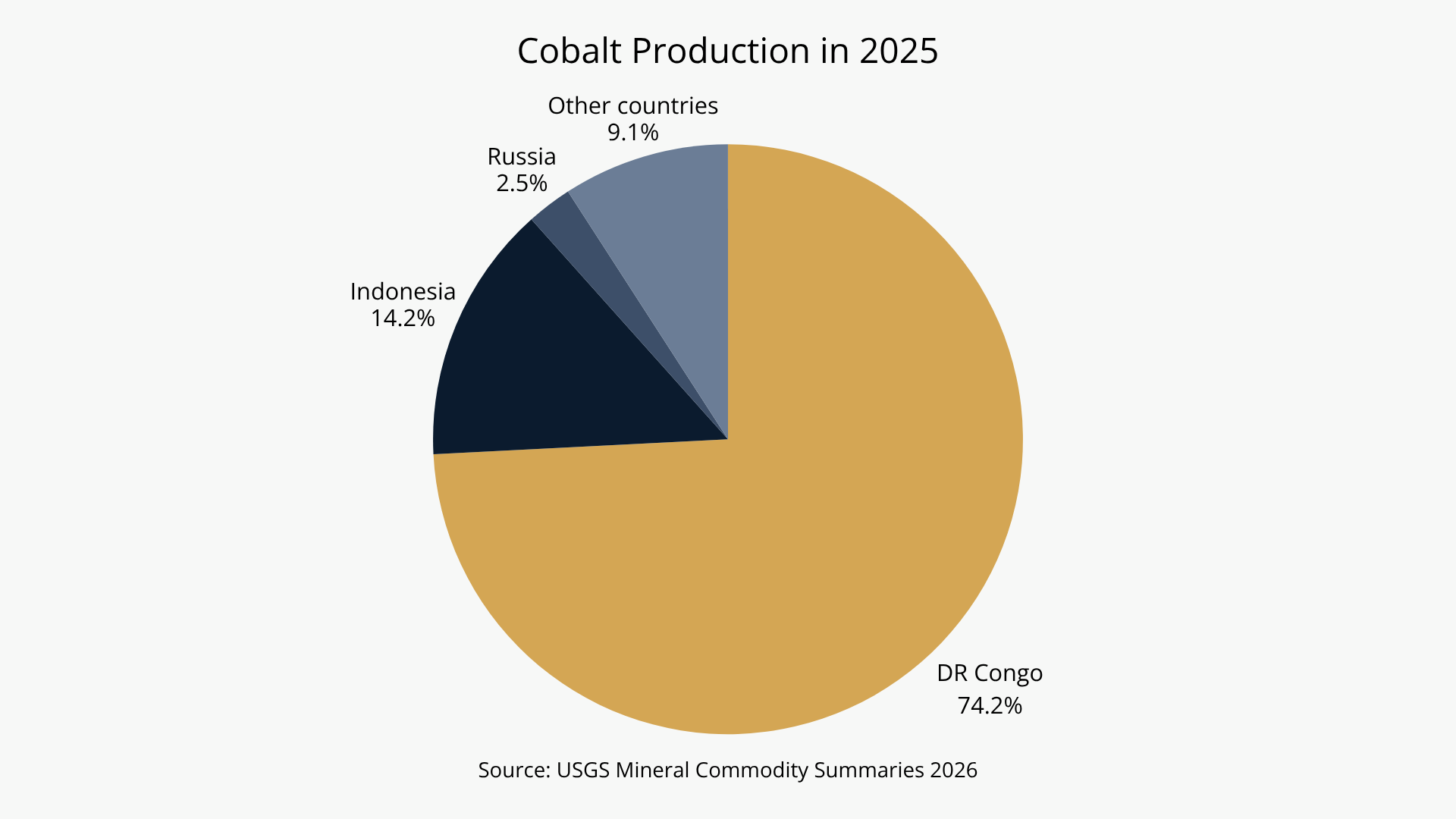

The DRC is central to the global supply of critical minerals used in modern industries. It produces approximately 70–75% of the world’s cobalt and is one of the leading sources of copper. Lithium production remains limited, but exploration is expanding: in March 2026, Zijin Mining Group announced a reported USD 1.5 billion lithium project in the country.

These minerals are essential not only for the energy transition (electric vehicles, energy storage, and grid infrastructure) but also for AI infrastructure, semiconductors, and advanced weapons systems. The International Energy Agency projects that, under stated policy scenarios, demand for cobalt could increase by 50–60% by 2040, copper by around 30%, and lithium could grow fivefold. This projected growth makes Congolese production both essential to global supply chains and increasingly subject to international competition.

Yet the DRC captures only a fraction of the value its minerals generate. Refining and processing take place overwhelmingly outside the country. Chinese firms alone absorb roughly 74% of Congolese cobalt exports and control an estimated 80% of global refining capacity. Beyond this downstream gap, Congolese authorities have increasingly come to view the fiscal and contractual terms governing extraction itself as disproportionately favourable to foreign operators.

This conviction has driven a sustained push to rebalance the terms of access. Since the late 2010s, the Congolese state has sought to capture a greater share of mining value, renegotiate legacy agreements, and diversify its international partnerships. Because China is by far the dominant foreign presence in the sector, this push for resource sovereignty has, in practice, meant renegotiating the terms of the relationship with Beijing.

“MINING FOR INFRASTRUCTURE”: THE DRC-CHINA DEAL UNDER INCREASED SCRUTINY

Chinese investment and the Sicomines model

China’s position in the DRC mining sector is the product of two decades of sustained engagement, combining upstream investment with downstream processing dominance. Chinese entities are estimated to account for a substantial majority of foreign participation in key mining assets. By some estimates, Chinese firms control approximately 80% of the DRC’s copper mines, reflecting a strategy of vertical integration across the value chain.

The cornerstone of this relationship is the 2008 “minerals for infrastructure” agreement concluded under President Joseph Kabila, structured through the Sicomines (short for La Sino-Congolaise des Mines) joint venture, owned 68% by a consortium of Chinese state-owned enterprises and 32% by Gécamines, the DRC’s state-owned mining company. The agreement granted Chinese partners mining rights in exchange for large-scale infrastructure investments, including roads, railways, hospitals, and universities.

While Sicomines is politically prominent, Chinese investment in the DRC mining sector also takes the form of conventional mining investments, governed by individual mining conventions.

CMOC Group (formerly China Molybdenum) operates Tenke Fungurume, one of the country’s largest copper-cobalt complexes, as well as the Kisanfu cobalt deposit. MMG, majority-owned by China Minmetals, operates the Kinsevere copper mine. Zijin Mining holds a major stake in the Kamoa-Kakula complex alongside Ivanhoe Mines. Norinco operates the Comica and Lamikal mines, and dozens of smaller concessions are held by Chinese firms.

The rest is for subscribers

Access the full analysis — legal framework, risk mapping, and practical implications — plus every issue of Lex Africana Mining Intelligence.